Table of Content

Say you want to add a home equity loan in the amount of $80,000 to the mix, and your lender requires you to preserve at least 20 percent equity. That’d bring your LTV ratio to 78.5 percent — below the 80 percent threshold your lender has limited you to. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Suzanne De Vita is the mortgage editor for Bankrate, focusing on mortgage and real estate topics for homebuyers, homeowners, investors and renters.

For example, if your home were to appraise for $420,000 and you still had $250,000 on your mortgage to pay off, you’d have $170,000 in equity and a loan-to-value ratio of 59.5 percent. The DTI ratio is a measure lenders use to determine whether you can reasonably afford to take on more debt. For a home equity loan, most lenders look for a DTI ratio of no more than 43 percent. For a conventional loan, Rocket Mortgage® requires a qualifying score of 620.

can i get a loan of 5000.00 to pay for my moms funrnal. i own my home and am willing to put it up for a loan

However, a good or excellent credit score will likely make you eligible for a competitive interest rate, assuming you meet the other eligibility criteria. If you put up assets to help someone secure a loan—whether it be your car or an expensive piece of jewelry—know that the bank can sell them to help pay off unpaid debts. Make sure you’re ready to handle that reality in a worst-case scenario.

The lender may be less reluctant to approve them, and they could lock in a great rate on the loan. A parent can step in and act as a co-signer or a co-borrower for their child to smooth the way to approval. A co-signer is someone who agrees to share joint responsibility for repaying a loan or a line of credit.

Best Personal Loans with Co-Signers Online For Good & Bad Credit

The lender will ask for some personal information from both of you, including your names, addresses and dates of birth. They will also need some financial information, such as your employment statuses and incomes. Keep in mind that the cosigner's income will matter more than the primary borrower's income during the application process. But they can be for much larger sums because the amount you can borrow is based on the value of your house minus the amount you have left to pay on the mortgage. So if your house is mostly paid off and is worth a lot of money, you could get a big loan. It's not common that someone would own a home yet have no credit history, but it is possible.

Of course, by the time a collection agency starts calling, there’s a good chance the overdue payments have already found their way onto your credit report. So despite the fact that you’re not even borrowing the money in any real sense, your credit could start to take a hit. All of a sudden, obtaining loans—or at least getting preferred interest rates—can become a big challenge. Of all the lenders that offer personal loans for cosigners, Lightstream and FreedomPlus are two of our favorites. Here’s a quick look at each of their standout features and how these two institutions compare to one another when it comes to cosigned loans.

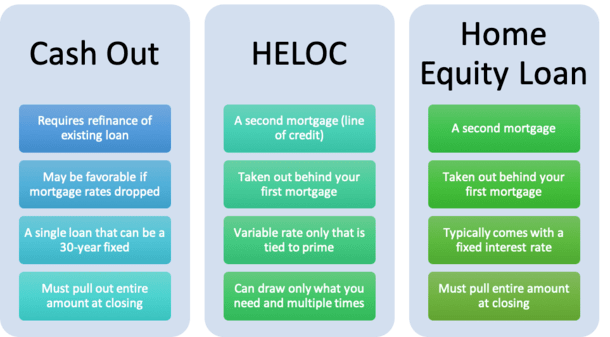

Common requirements for a home equity loan and a HELOC

Were this not the case, having a cosigner on the loan—regardless of how high their credit score—wouldn’t matter much to the bank. But because the lender knows it can go after cosigners for overdue payments, that second signature can make a world of difference in the loan approval process. By cosigning the loan, you are not taking the loan out for yourself, but you promise to repay the loan if the borrower cannot. Although the debt isn't technically yours, it still appears on your credit report. This may affect your ability to borrow money for yourself in the future.

The potential downside of getting a personal loan with a co-signer is that you can damage their credit if you miss a payment or default. Before you ask someone to cosign, inform them of the risks and make sure they understand their rights as a co-signer. Our advertisers do not compensate us for favorable reviews or recommendations. Our site has comprehensive free listings and information for a variety of financial services from mortgages to banking to insurance, but we don’t include every product in the marketplace.

Yes — in fact, this is the rule for any type of loan you’d like to borrow, including a home equity product. It can be tough to find someone who’s willing to commit to a loan, however, and you’ll still need to qualify for it based on your individual credit. Think of a co-signer as someone who can help strengthen your loan application and increase your chances of approval, rather than someone whose good credit means yours gets overlooked.

This law changed some of the rules for deducting home equity loan interest and caused some confusion. As of 2018, taxpayers can deduct the interest paid on a home equity loan amount up to $750,000. The law only allows this deduction if you used the loan money to make improvements or repairs to the home.

While we do our best to ensure our information is up to date and calculations are accurate, all information is presented without warranty. If you find information or calculations you believe to be in error, please contact us. Estimated interest rate, APR, and other terms are not binding in any way. Your actual interest rate and APR will depend on factors like credit score, requested loan amount, loan term, and credit history. Only borrowers with excellent credit will quality for the lowest rate.

Getting a home equity loan with bad credit isn’t impossible, though. Once the loan is closed, both you and the co-signer are on the hook for the payments. It doesn't matter to the lender whether one or both of you make the payments as long as they're paid. If you fail to make the payments, however, it can take legal action against both of you. If, eventually, you wish to remove the co-signer, you will have to prove that you can afford the payments on your own. If the lender determines the co-signer is no longer needed, you'll have to sign a modification or an entirely new set of documents depending on the lender's policy and procedure.

If the borrower doesn’t pay, the cosigner is obligated to pay any missed payments or even the full amount of the loan. If you have a mistake on your report, such as an incorrect balance reported, it could drop your credit score. That said, we found two lenders that allow you to take out a personal loan with a co-signer. If you can, try to find a co-signer who doesn’t have a lot of debt relative to their income. Lenders sometimes have minimum DTI ratio requirements — the total debt you owe versus your monthly gross income. For example, if your monthly debt is $1,000 and your gross monthly income is $2,000, then your DTI ratio is 50 percent.

Also, set up alerts that notify you the moment your credit score drops. Here are the steps to take to apply for a home equity loan if you don't have good credit. You may co-sign for a HELOC, however, you won't be automatically added to the deed. A co-signer assumes full responsibility without ownership rights. Each bank has a minimum home equity loan amount, which varies from one bank to another. It's important to understand all the details of using a home equity loan or HELOC for debt consolidation before deciding to take one out.

No comments:

Post a Comment